Stuff happens. I know you don’t think it will happen to you, but it can. I have consulted hundreds of people who were hit by a totally unexpected peril that they never saw coming. Their house burnt down. They become disabled. They get sued and liable for a huge loss. They die. These perils are tragic and can also be devastating to your personal finances. A lifetime of financial success can be lost in a single unlucky event. While it may be impossible to prevent these events from ever happening you can at least protect your finances from being devastated as well.

Insurance is a great way to manage your personal finance risk. Insurance premiums can be expensive but some insurance you can’t afford to be without.

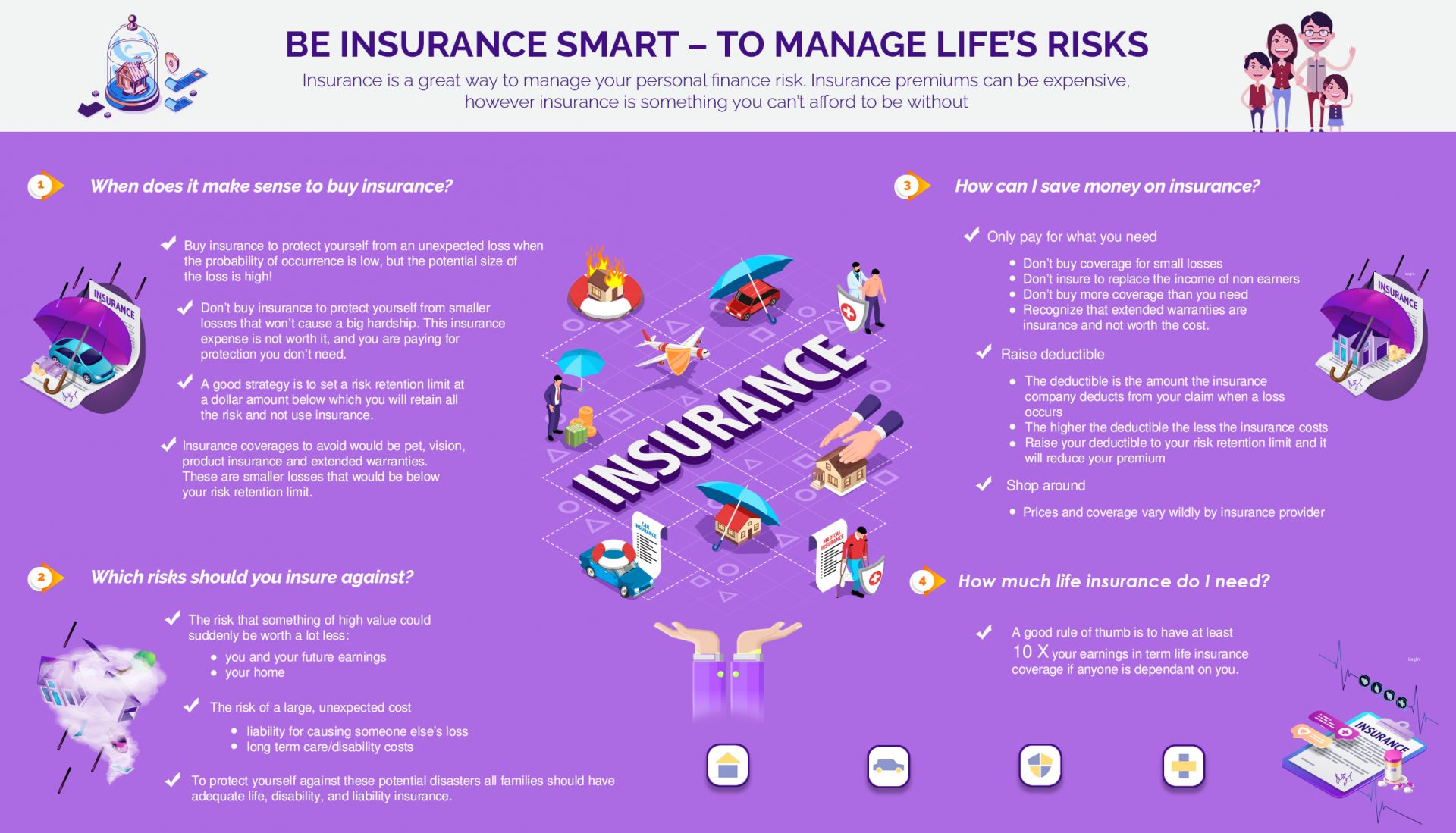

Buy insurance to protect yourself from an unexpected loss when the probability of occurrence is low, but the potential size of the loss if high!

Don’t buy insurance to protect yourself from smaller losses that won’t cause a big hardship. This insurance expense is not worth it, and you are paying for protection you don’t need.

A good strategy is to set a risk retention limit at a dollar amount below which you will retain all the risk and not use insurance.

Insurance coverages to avoid would be pet, vision, product insurance and extended warranties as these are smaller losses that would be below your risk retention limit.

The risk that something of high value could suddenly be worth a lot less:

- you and your future earnings

- your home

The risk of a large, unexpected cost:

- liability for causing someone else’s loss

- long term care/disability costs

To protect yourself against these potential disasters all families should have adequate life, disability, and liability insurance.

A good rule of thumb is to have at least 10 X your earnings in term life insurance coverage if anyone is dependent on your income.

Only pay for what you need.- Don’t buy coverage for small losses

- Don’t insure to replace the income of non-earners.

- Don’t buy more coverage than you need

- Recognize that extended warranties are insurance and not worth the cost.

Raise deductibles- The deductible is the amount the insurance company deducts from your claim when a loss occurs

- The higher the deductible the less the insurance costs

- Raise your deductible to your risk retention limit and it will reduce your premium

Shop around

- Prices and coverage vary wildly by insurance provider.

- Look for discounts by bundling different policies.